Flood risk can affect a property’s safety, insurance costs, and long-term value. Before you buy, you should check whether the home sits near rivers, the coast, or low-lying ground that can collect surface water after heavy rain.

A quick review of official flood maps, past flood history, and local drainage issues can reveal risks that a viewing will not show. You can then compare properties, plan protection measures, and avoid costly surprises after completion.

Key takeaways

- Check river, coastal, surface water, and groundwater flood risk separately.

- Use official flood maps early, before making an offer or booking surveys.

- Ask the seller for past flooding details, including dates, depth, and repairs.

- Review the property’s elevation, nearby watercourses, and local drainage history.

- Order conveyancing searches that flag flood risk and past insurance claims.

- Get insurance quotes before exchange; high premiums can affect affordability.

- Factor in resilience measures, like flood doors, airbrick covers, and raised electrics.

What Flood Risk Means for Homebuyers (Rivers, Surface Water, Groundwater, Coastal)

In England, around 5.2 million properties are in areas at risk of flooding from rivers, the sea, or surface water. That number matters because “flood risk” is not one hazard. It is a mix of sources that behave differently, affect insurance in different ways, and can change with local drainage or coastal defences.

River flooding (fluvial) happens when watercourses overtop after sustained rainfall upstream. Surface water flooding (pluvial) comes from intense rain that overwhelms drains and runs downhill, even far from a river. Groundwater flooding occurs when the water table rises and pushes water up through soil, often lasting longer than a single storm. Coastal flooding is driven by high tides, storm surges, and wave action, and it can worsen when sea levels rise.

Risk ratings also reflect probability. The Environment Agency commonly describes “high” risk as a chance of flooding greater than 3.3% each year (more than 1 in 30), while “medium” sits between 1% and 3.3% (1 in 100 to 1 in 30). When you are buying a house in a mapped risk area, treat the source and the probability as separate questions, because each points to different checks and costs.

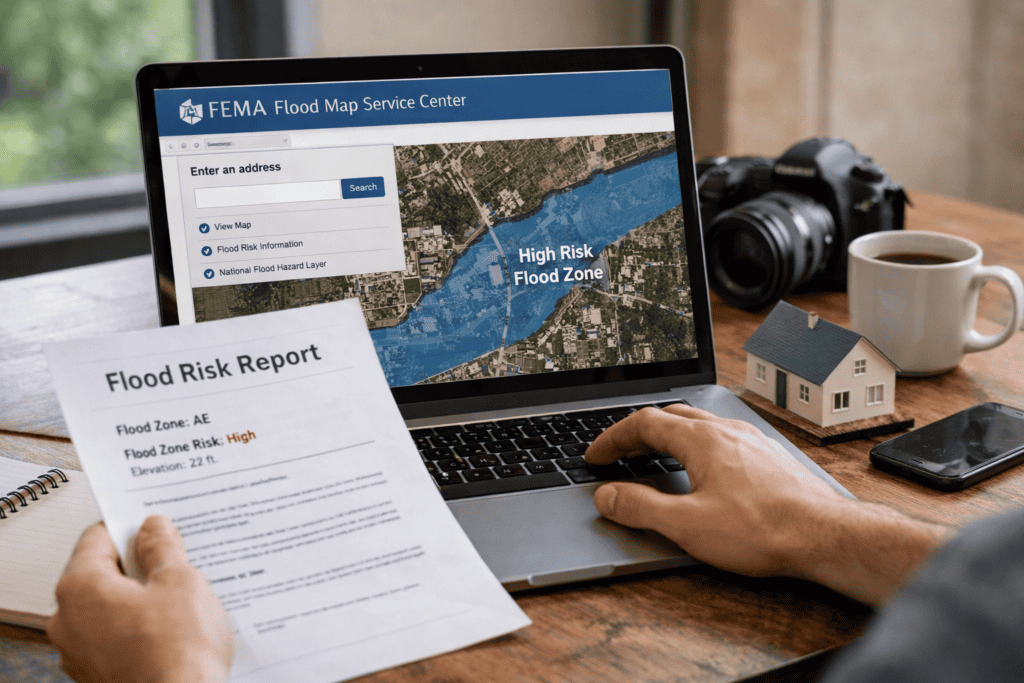

Check the UK Flood Maps and Data Sets Before You View a Property

UK flood maps separate hazards, and each one can change your risk profile. River and sea maps focus on watercourses and coastal surges. Surface water maps show where heavy rain can overwhelm drains and flow downhill. Groundwater mapping can matter in chalk or clay areas where water rises after long wet periods.

Use these sources before you view:

- GOV.UK Check long term flood risk (England): postcode-level results for rivers/sea, surface water, groundwater, and reservoirs.

- Flood Map for Planning (England): more technical layers used for planning decisions.

- SEPA Flood Maps (Scotland).

- Natural Resources Wales Flood Map (Wales).

- Flood Maps NI (Northern Ireland).

Bring screenshots to the viewing. Ask the agent to confirm the exact address and boundary, then check whether the flagged areas sit on the building, garden, or access route.

Review the Property’s Flood History and Local Drainage Issues

Flood maps show predicted risk, while flood history shows what has actually happened. Both matter, but they answer different questions. History can reveal repeat problems from blocked gullies, undersized culverts, or a low point in the road that holds water after heavy rain.

Option A is desk-based checks: search the HM Land Registry listing history for past flood-related disclosures, review local news archives, and ask the local council about recorded highway flooding and gully maintenance. Option B is on-site evidence: look for tide marks on brickwork, replaced lower plaster, raised sockets, air-brick covers, or non-return valves on waste pipes.

| Check | Option A: Records | Option B: Physical signs | What it changes |

|---|---|---|---|

| Past flooding | Disclosures, reports, news | Staining, repairs, altered finishes | Negotiation and survey focus |

| Drainage performance | Council maintenance history | Ponding, silt, blocked gullies | Likelihood of surface water issues |

| Neighbour experience | Written enquiries | Visible flood barriers | Insurance and resilience costs |

If records and signs disagree, treat the risk as unresolved and ask your solicitor to raise targeted enquiries before exchange.

Get a Flood Risk Search and Understand What the Report Covers

A viewing can hide a measurable risk: a property may sit in a “low” map zone yet still trigger higher insurance premiums or exclusions after a formal search. A flood risk search pulls multiple data sets into one report, letting you compare river, surface water, groundwater, and reservoir indicators in one place.

Order the search through your conveyancer or a regulated search provider, then check what the report covers. Most reports include a risk rating, modelled flood extents, and notes on nearby defences or watercourses. Check whether the report flags “further action” and whether it separates property-level risk from road or garden flooding.

Next, match findings to decisions. Ask your insurer for a quote using the full address and any report reference. If the report shows surface water sensitivity, plan measures early, such as how to prevent your house from flooding with door barriers, airbrick covers, and drainage maintenance.

When the report is clear and insurable, you cut the chance of late surprises, renegotiations, or a failed mortgage condition tied to flood exposure.

Ask the Right Questions During Viewings and Surveys (Seller, Agent, Surveyor)

In England, Defra reports around 5.2 million properties are in areas at risk of flooding from rivers, the sea, or surface water. That scale means a viewing should test claims, not rely on reassurance. A seller may describe “no issues”, while a surveyor may spot past water entry or weak drainage details.

Use the viewing to gather facts you can verify later. Ask for dates, documents, and what changed after any incident. If answers stay vague, treat that as a risk signal and push for evidence.

- Seller: Has any part of the home, garden, garage, or access road flooded in the last 10 years? What was the depth (in cm) and how long did water remain?

- Agent: Are there known issues on the street after heavy rain, and have any sales fallen through due to flood searches or insurance quotes?

- Surveyor: Check for tide marks, replaced plaster at low level, raised sockets, air brick covers, non-return valves, and damp patterns that do not match condensation.

- Paperwork: Request any flood resilience invoices, guarantees, or photos. Confirm whether the property has ever been refused insurance, or faced a large excess (for example, £1,000+).

Bring the questions to the survey briefing so the inspection covers the right areas, including thresholds, air bricks, and external ground levels.

Decide What to Do If Risk Shows Up (Insurance, Costs, Resale, Walk Away)

A buyer agrees a price on a ground-floor flat after a survey, then the conveyancer’s flood search flags “significant” surface water risk on the access road. The lender still offers a mortgage, but the buyer’s insurer quotes a high premium and a large flood excess. The buyer now has a decision to make before exchange.

Start with insurance. Get quotes using the exact address and ask what drives the price: flood excess, exclusions, or limits on alternative accommodation. If the home is built before 1 January 2009, check eligibility for Flood Re, which can make cover more available for some homes.

Next, price the practical costs. A higher excess can shift risk back to you, so budget for emergency savings and resilience work. Then think about resale: future buyers and lenders will run the same searches. If the numbers do not stack up, renegotiate, request evidence of past mitigation, or walk away before you become committed.

Frequently Asked Questions

What types of flooding can affect a property in the UK?

UK properties can face river flooding (from rivers), coastal flooding (sea surges and high tides), surface water flooding (heavy rain overwhelming drains), groundwater flooding (rising water tables), and sewer flooding (overloaded or blocked sewers). Some homes also face reservoir or canal breach flooding, although this is less common.

Which official flood maps can you use to check flood risk before buying a home?

You can check official flood maps from the relevant national agency: the Environment Agency Flood Map for Planning (England), Natural Resources Wales Flood Map, SEPA Flood Maps (Scotland), and the Department for Infrastructure Flood Maps (Northern Ireland). Use surface water, river, and coastal layers to review each risk type.

How do you interpret flood zones and risk categories shown on flood maps?

Flood maps group land into zones based on flood chance. Read the legend, then match the property to its zone. “High risk” zones often mean a 1% annual chance of river flooding (1-in-100) or a 0.2% chance (1-in-500). “Medium” and “low” indicate lower odds, not zero. Check if the home sits inside the boundary.

What information does a flood risk search in conveyancing include, and what does it not include?

A conveyancing flood risk search usually flags river, coastal, surface water and groundwater risk, past flood indicators, and whether flood defences may affect risk. It may also note nearby watercourses and broad insurance implications. It does not confirm a property has flooded, guarantee future flooding, replace a site survey, or assess internal drainage and maintenance.

What questions should you ask the seller or estate agent about past flooding and flood defences?

Ask whether the property, garden, garage, or access road has ever flooded, and the dates, depth, and cause (river, surface water, sewer, groundwater). Request copies of insurance claims, repairs, and any survey reports. Confirm what flood defences exist (airbrick covers, barriers, pumps), who maintains them, and whether any warnings or evacuation notices were issued.

How can flood risk affect home insurance availability, premiums, and excesses?

Flood risk can limit which insurers will offer cover, especially for homes with past claims or high-risk postcodes. When cover is available, premiums often rise and insurers may add flood exclusions. Excesses can also increase, meaning you pay more towards a flood claim. Some policies set a separate, higher flood excess.

When should you commission a specialist flood risk assessment before exchanging contracts?

Commission a specialist flood risk assessment before exchanging contracts if searches flag high or medium risk, the property sits near a river, coast, reservoir, or surface water flow path, or the seller reports past flooding. Arrange it early enough to renegotiate price, request flood resilience measures, or withdraw without penalty.